The Minefield of Construction Insurance

Let’s be honest – construction is one of the riskiest businesses out there. Between heavy machinery, towering scaffolding, and tight deadlines, there’s always something that can go wrong. And when things do go sideways, the insurance claims can be massive. But here’s the kicker: even if you think you’re covered, there might be a sneaky little provision in your policy that could leave you high and dry when you need protection most.

I’m talking about something called “Action Over Exclusion” – and trust me, it’s not as boring as it sounds. This little-known insurance provision has been the silent destroyer of construction businesses nationwide, particularly those operating in states like New York. If you’ve never heard of Action Over Exclusion before, you’re not alone. But by the time you finish reading this, you’ll understand why it’s one of the most critical things to look out for in your Commercial General Liability (CGL) policy.

Here’s why this matters to your bottom line: these exclusions can cost you millions. We’re not talking about small change here – Action Over Exclusion gaps have left countless contractors facing devastating financial exposure that they never saw coming. It’s like having an insurance policy with a giant hole right in the middle of it.

So what are you going to learn today? We’re going to dive deep into what Action Over Exclusion means, why it’s fierce for contractors (especially those dealing with New York’s infamous “Scaffold Law”), who gets hit hardest by these exclusions, and most importantly, what you can do to protect yourself. By the end of this post, you’ll have a game plan to identify these coverage gaps and close them before they can sink your business.

What Exactly is Action Over Exclusion?

Alright, let’s break down Action Over Exclusion in plain English. At its core, this is a provision in your CGL policy that says, “Hey, if one of your employees gets hurt and sues someone else, and that someone else comes after you for compensation, you’re on your own.”

Now, let me paint you a picture of how this whole Action Over Exclusion mess typically unfolds:

Normally, when your employee gets injured on the job, they can’t just sue you directly – that’s what Workers’ Compensation is for. It’s like an unspoken agreement: your employee gets their medical bills covered and some compensation, but they give up the right to take you to court. Pretty straightforward, right?

But here’s where things get tricky. That injured employee can sue other parties they think were negligent – maybe the general contractor, the property owner, or even the manufacturer of faulty equipment. And when they do, these third parties often have contracts with you that say something like, “If we get sued because of your work, you’ve got to hold us harmless and cover our costs.”

This is where Action Over Exclusion rears its ugly head. Even if that building owner or general contractor is listed as an additional insured on your policy, the exclusion can still leave them completely exposed. It’s like telling them, “Sorry, you’re named on our policy, but we’re not going to protect you when the chips are down.”

You might also hear this called “action over coverage,” “Labor Law coverage,” “scaffold law coverage,” or “third-party action over” – especially when contractors are talking about New York insurance. They’re all basically referring to the same thing: whether your policy will step up when someone comes after you or your additional insureds for workplace injury claims.

Why Action Over Exclusion is a Contractor’s Nightmare

Let me tell you why Action Over Exclusion keeps contractors up at night. First off, it creates these massive coverage gaps that shift all the financial risk from your insurance company straight onto your shoulders. When your insurer walks away because of this exclusion, guess who’s left holding the bag? That’s right – you are.

But it gets worse. Having an Action Over Exclusion in your policy is like wearing a sign that says, “I’m not a reliable business partner.” When you present a policy with this exclusion to a general contractor or building owner, you’re telling them you’ll leave them high and dry if there’s a problem. And trust me, they’re incredibly sensitive to this kind of exposure. Most experienced GCs and property owners have been burned before, and they’re not about to take that risk again.

This directly impacts your ability to win bids and maintain business relationships. Why would a general contractor choose you when your competitor offers the same services but with insurance that protects them?

Now, if you’re working in New York, things get even more complicated thanks to something called the “Scaffold Law” – specifically, Labor Laws 240 and 241. This is some seriously antiquated legislation from 1885 that creates absolute havoc for everyone involved in construction. Under this law, general contractors and property owners face “absolute liability” for gravity-related injuries like falls or objects dropping on workers.

What does absolute liability mean? It means these parties can be held responsible even if they did everything right, provided all the safety training, supplied proper equipment, and followed every regulation to the letter. If someone falls or gets hit by a falling object, the GC and property owner are automatically on the hook. It’s no wonder New York contractors pay up to 10 times more for insurance than contractors in other states!

This creates what I call the “very liberal states effect.” In places like New York and Miami, you’ll see personal injury attorneys aggressively advertising to injured workers, encouraging them to file lawsuits. It’s become such a hot topic that it’s fundamentally changed how construction insurance works in these markets.

And here’s another nightmare scenario: many smaller subcontractors find it almost impossible or cost-prohibitive to get general liability insurance without an Action Over Exclusion. This forces larger contractors to effectively assume their subs’ actions over risk on their balance sheet. You’re not just managing your exposure – you’re taking on everyone else’s too.

Who is Most Affected by Action Over Exclusions?

The Action Over Exclusion doesn’t discriminate – it impacts pretty much everyone in the construction food chain, but some get hit harder than others.

General contractors are probably the biggest targets. They’re the ones getting sued left and right in third-party lawsuits, and they’re usually contractually obligated to indemnify property owners. When their subcontractors have Action Over Exclusions, it creates a direct threat to the GC’s financial stability.

Property owners and building owners face their own set of problems. They’re often the first ones to get sued when a worker gets injured, and they’re counting on their contractors’ insurance policies (where they’re listed as additional insureds) to provide defense and indemnification. But if there’s an Action Over Exclusion, that protection might not be there when they need it most.

Subcontractors are in a weird position. While the exclusion is technically on their policy, the financial consequences often bounce right back to them or the general contractor they’re working for. Plus, having this exclusion can seriously impact their ability to land jobs with insurance-savvy GCs.

Even injured employees play a role in this whole mess. While they’re covered by Workers’ Compensation for their direct injuries, they’re the ones who kick off the “action over” scenario when they file lawsuits against third parties.

Real-World Implications: Case Study Insight

Let me share a case that illustrates how courts interpret this stuff: Gilbane Building Co. v. Empire Steel Erectors from 2010. This case is a perfect example of how tricky policy language can be and why every word matters in your insurance contract.

Here’s what happened: An employee of a subcontractor got injured and sued the general contractor, Gilbane. Gilbane then went to the subcontractor’s insurance policy, where they were listed as an additional insured, expecting coverage for the lawsuit.

Now, here’s where it gets interesting. The court ruled in favor of providing coverage, even though the lawsuit didn’t explicitly blame the subcontractor for the accident. The court said that as long as there was a plausible connection between the subcontractor’s work and the injury, coverage should apply. They also made a crucial point: when policy language is ambiguous, it should be interpreted in favor of providing coverage, not denying it.

The key takeaway from this case is that policy language matters immensely. Details like whether the exclusion uses phrases like “caused in whole or in part” can make or break your coverage. This case shows why you absolutely must carefully review your policies and not just assume you understand what they say. The devil is definitely in the details, and those details can save or cost you millions.

Practical Strategies to Mitigate Risks & Close Coverage Gaps

Okay, now that I’ve probably scared you sufficiently, let’s talk solutions. The good news is that there are concrete steps you can take to protect yourself from Action Over Exclusion nightmares.

1. Conduct a Comprehensive Policy Review

First things first – you need to get intimate with your insurance policy. I mean, intimate. Don’t just flip through it like you’re reading the Sunday paper. Frank Franzini from Posillico Civil Inc. puts it perfectly: Don’t just collect Certificates of Insurance (COIs) and call it a day. You need to read the policy and all the endorsements.

Look specifically for exclusions related to employee injuries and indemnity agreements. These are the sections where Action Over Exclusions like to hide. Also, make sure your coverage limits are sufficient for the potential high-cost claims you might face. Remember, we’re talking about potentially millions of dollars in exposure here.

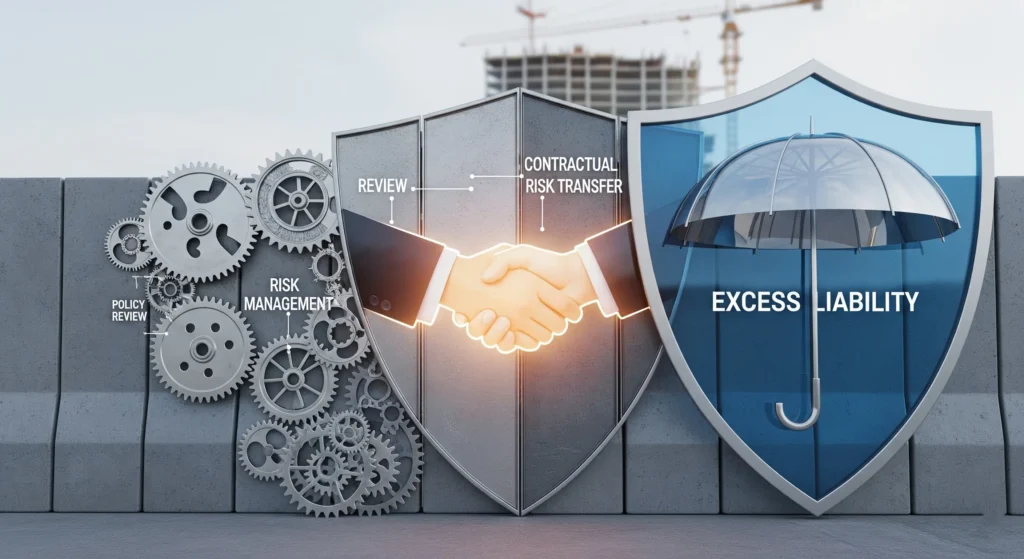

2. Add Supplemental Coverage

Sometimes the best defense is a good offense. Consider adding umbrella or excess liability policies to your insurance portfolio. These policies provide additional limits that can help fill gaps left by exclusions in your primary policy. It’s like having a backup parachute when you’re skydiving – you hope you never need it, but you’ll be really glad it’s there if you do.

You might also want to look into tailored endorsements like Owners and Contractors Protective Liability (OCP) or specific Additional Insured endorsements designed for your type of operations. These can provide targeted coverage for scenarios that standard policies might exclude.

3. Strengthen Contractual Risk Transfer

This is where you get smart about how you structure your contracts. Implement clear, robust indemnity clauses in your agreements with subcontractors. These clauses should appropriately transfer liability risks so you’re not left holding the bag when something goes wrong.

Here’s a crucial strategy: mandate that your subcontractors carry adequate coverage, including policies without Action Over Exclusions. Posillico does this religiously – they make sure all their subs meet strict insurance requirements to prevent potential claims from coming back to bite them. It might seem harsh, but it’s necessary protection in today’s lawsuit-happy environment.

4. Implement Robust Risk Management Practices

Prevention is always better than a cure. The best way to deal with Action Over Exclusion issues is to reduce the likelihood of workplace injuries in the first place. This means implementing comprehensive safety training programs and maintaining strict compliance with all regulations.

Posillico is a great example of this philosophy in action. They prioritize employee safety so seriously that they’ll invest in more expensive equipment, like cut-resistant gloves, if it means keeping their workers safer. That upfront investment pays dividends when it comes to reducing claims and maintaining reasonable insurance costs.

Set up continuous claims monitoring to review your claims data regularly. Look for trends that might indicate systemic issues you can address. Also, make sure everyone on your team understands governmental regulations and company policies. Prevention starts with education.

Before starting any project, conduct a comprehensive Risk Management Evaluation. Get your project management, safety, compliance, and finance teams all on the same page about potential issues and compliance goals. It’s much easier to prevent problems than to deal with them after they’ve already occurred.

5. Consider Captive Insurance Programs

For contractors, especially those dealing with New York’s challenging insurance market, group captive insurance programs can be a game-changer. This is where multiple companies band together to form their own insurance company, providing coverage when traditional commercial insurance with Action Over Exclusions becomes cost-prohibitive or simply unavailable.

The benefits of this approach are significant. It protects your parent company’s balance sheet and insurance program from subcontractor losses, and it’s funded by the money you save from not purchasing overpriced commercial insurance. It’s like forming your exclusive insurance club where everyone understands the unique challenges of construction work.

Partnering with the Right Insurance Experts

Here’s something I can’t stress enough: you need to work with insurance professionals who really understand the construction industry. This isn’t the time to go with your cousin’s friend who sells car insurance on weekends. You need someone with deep experience in General Liability policies and a thorough understanding of challenging markets like New York.

The right insurance expert will know where to find policies without Action Over Exclusions. For example, some admitted carriers offer artisan contractor Business Owner Policies (BOPs) without these exclusions, depending on your state and the specific type of work you do. Companies like Merchants, Utica National (outside NYC), Security Mutual, and Main Street America are worth exploring.

A good insurance professional will also stay on top of changing regulations and market conditions. The construction insurance landscape is constantly evolving, and you need someone who’s actively monitoring these changes and adjusting your coverage accordingly.

Conclusion

Let’s bring this all together. Understanding and proactively addressing Action Over Exclusion isn’t just some nice-to-have knowledge – it’s critical for the financial health and operational continuity of any construction business. These exclusions represent some of the biggest hidden risks in your insurance portfolio, and ignoring them can put your business out of business.

But here’s the empowering part: proper protection is achievable with the right strategies and knowledge. You don’t have to be a victim of these coverage gaps. By conducting thorough policy reviews, implementing robust risk management practices, strengthening your contractual protections, and working with experienced insurance professionals, you can close these gaps and get back to focusing on what you do best – building great projects.

The construction industry will always be risky, but with the right approach to Action Over Exclusion, you can make sure those risks don’t sink your business. Knowledge is power, and now you know how to protect yourself and your company.

Ready to Enhance Your Protection?

Don’t let Action Over Exclusion catch you off guard. The time to address these coverage gaps is now, before you’re facing a million-dollar lawsuit with inadequate protection. I strongly encourage you to consult with an experienced construction insurance professional for a comprehensive review of your current policies and tailored solutions that address your specific risks.

Your business deserves protection that works when you need it most. Take action today to ensure your insurance portfolio is working for you, not against you.

Frequently Asked Questions

Q: What is the “Scaffold Law” (New York Labor Law 240 & 241)?

A: It’s an antiquated New York law dating back to 1885 that imposes “absolute liability” on property owners and general contractors for “gravity-related” injuries like falls or falling objects. This means they can be held responsible regardless of fault, even if they provided all proper safety training and equipment.

Q: Can employees sue their employers for work-related injuries?

A: Typically, no. Employees are usually precluded from suing their employers directly due to Workers’ Compensation statutes, which provide coverage for workplace injuries. However, they can sue other potentially negligent third parties like general contractors, property owners, or equipment manufacturers.

Q: Does being an “additional insured” guarantee coverage if there’s an Action Over Exclusion?

A: Unfortunately, no. If a policy includes an Action Over Exclusion, coverage may still be denied to the building owner or general contractor even if they have a certificate naming them as an additional insured. The exclusion can override the additional insured status.

Q: How does an Action Over Exclusion impact a subcontractor’s ability to get work?

A: Significantly. Many general contractors and project owners are “insurance smart” and will actively avoid working with subcontractors whose policies include Action Over Exclusions, as it leaves them financially exposed. This exclusion can be a major barrier to winning contracts.

Q: What is a captive insurance program in the context of construction?

A: A captive insurance program is when multiple companies form their own insurance company to cover specific risks. In construction, it’s often used by contractors to manage contractual liability assumed from underinsured subcontractors, especially for Action Over risks. This approach can be more cost-effective than traditional commercial insurance with exclusions and provides more control over coverage terms.

")