Okay, so you’ve typed “look insurance” into Google and ended up here. Maybe you’re hunting for that specific Look Insurance Agency everyone’s been talking about, or perhaps you’re just trying to figure out how the heck to find decent insurance without losing your mind. Either way, I’ve got your back!

Let’s be real – shopping for insurance is about as fun as watching paint dry, but it’s one of those adulting things we can’t avoid. The good news? Once you know what you’re doing, it’s not that scary. Plus, finding the right coverage can save you serious cash and a ton of headaches down the road.

Understanding “Look Insurance”: Brand vs. Action

Here’s the thing – when you search “look insurance,” you might be looking for two different things. It’s like when you Google “apple” – are you hungry or shopping for a phone? Same deal here.

Are You Looking for Look Insurance Agency?

So there’s a company called Look Insurance Agency, and they’re pretty solid from what I can tell. They’ve got offices mainly in Michigan and Florida, and they’re what we call an “independent agency” (more on that later – it’s a big deal).

These folks handle all the usual suspects: car insurance, home insurance, business coverage, and life insurance. What’s cool about them is they’re not tied to just one big insurance company, so they can shop around for you. It’s like having a personal shopper, but for insurance instead of shoes.

They’ve got decent reviews on Yelp, and they’re hanging out with the Better Business Bureau, which is always a good sign. If you’re specifically looking for these guys, you can usually get quotes through their website or just give them a call. Pretty straightforward stuff.

But here’s the kicker – if Look Insurance Agency is what you’re after, you might want to stick around anyway. Even if you end up going with them, knowing how to evaluate ANY insurance company is gonna make you a much smarter shopper.

Or Are You Looking for Insurance? 5 Steps to Find the Perfect Coverage

If you landed here because you’re trying to figure out how to find good insurance (and not get ripped off in the process), you’re in the right place. I’m gonna walk you through five steps that’ll turn you into an insurance-shopping ninja:

Step 1: Figure out what you need (spoiler: it’s probably not what you think) Step 2: Learn where to shop – and trust me, not all insurance agents are created equal Step 3: Master the art of comparing quotes like a pro (hint: cheapest isn’t always best) Step 4: Read the fine print (I know, I know, but it matters) Step 5: Know what to expect when stuff goes wrong and you need to file a claim

Ready? Let’s dive in!

Step 1: Assessing Your Needs – What to Look for in a Policy

Alright, first things first – you gotta figure out what you need before you start shopping. I see way too many people just grabbing whatever’s cheapest and then getting burned when something bad happens. Don’t be that person.

Evaluating Your Personal & Financial Situation

Think of this like dating – you wouldn’t use the same approach if you’re 22 and single versus 35 with two kids and a mortgage, right? The same goes for insurance.

Start by making a list of all your stuff. Your car, your house (or apartment), any fancy electronics, jewelry, whatever. If losing it would make you cry (or broke), it probably needs insurance.

Here’s a reality check: if people depend on your paycheck, you need life insurance. The old rule says get coverage worth about 10-12 times what you make in a year. Sounds like a lot? It is, but think about it – if something happens to you, your family still needs to eat, pay the mortgage, and maybe send kids to college someday.

Now, about deductibles – this is how much you pay out of pocket before insurance kicks in. Higher deductible = lower monthly payment, but make sure you can actually afford that deductible if something happens. There’s no point saving $20 a month if you can’t come up with $1,000 when your car gets dinged up.

Oh, and where you live matters more than you’d think. Live in tornado alley? You’ll need different coverage than someone chilling by the beach (who might need flood insurance instead). City folks might need higher liability limits because, let’s face it, people sue more in busy places.

Key Types of Insurance to Consider

Car Insurance is the big one since it’s legally required almost everywhere. Don’t just get the bare minimum – that’s like bringing a water gun to a firefight. If your car’s worth anything, get comprehensive and collision coverage too. And if you’re still paying off your car loan? Gap insurance might save your butt if your car gets totaled.

Home/Renters Insurance is super important, but here’s what most people don’t realize – if you’re renting, your landlord’s insurance doesn’t cover YOUR stuff. All those clothes, electronics, furniture? You need your coverage. And homeowners, make sure your coverage reflects what it would actually cost to rebuild your house today, not what you paid for it.

Life Insurance comes in two flavors: term (cheaper, covers you for a set time) and whole life (more expensive, but builds cash value). For most people, term life is the way to go, especially when you’re younger and money’s tight.

Business Insurance – even if you just have a side hustle or work from home, don’t assume you’re covered. Most regular homeowners’ policies won’t cover business stuff, and that could leave you in a really bad spot.

Step 2: Where to Look – Independent Agents vs. Captive Agents vs. Direct

This is where it gets interesting. Not all ways of buying insurance are the same, and honestly, most people have no clue about the differences. Let me break it down for you.

The Power of Choice: Why Independent Insurance Agents Offer More Options

Independent agents are like the Switzerland of insurance – they’re neutral. They work with a bunch of different insurance companies, so they can shop around for you instead of just trying to sell you whatever Company X is pushing this month.

Here’s why this rocks: if you get in an accident or have a claim, your independent agent is on YOUR side, not the insurance company’s. They want to keep you happy because their business depends on it, not because some corporate overlord is breathing down their neck.

These agents also tend to stick around and get to know you. They’ll call when it’s time to review your coverage, help you figure out if you need more (or less) insurance as your life changes, and fight for you if the insurance company tries to lowball a claim.

Plus, many independent agencies offer extras like business consulting or help with employee benefits if you’re a business owner. It’s like having an insurance concierge.

The Captive Agent: Working for a Single Brand

Captive agents work for just one company – think your neighborhood State Farm or Allstate agent. The upside? They know their company’s products inside and out, and they usually get great training on how everything works.

The downside? They can only sell you what their company offers. It’s like going to a Ford dealer when you might need a Honda. They might have great cars, but what if Ford just doesn’t make what you need?

Some of these big companies do have competitive rates and cool features you can’t get elsewhere, so don’t write them off completely. Just know that you’re not getting the full picture of what’s available.

Going Direct: The Pros and Cons of Buying Online

Buying insurance online is super convenient – you can do it in your pajamas at 2 AM if you want. Companies like Geico and Progressive have made it pretty easy, and you might save some money since there’s no agent commission.

This works great if you’re comfortable with technology and have pretty straightforward needs. Basic car insurance or renters insurance? You can probably handle that online, no problem.

But here’s the catch – you’re on your own. No one’s gonna call and remind you that you should probably increase your coverage when you buy a new car or move to a different state. And when you need to file a claim? You’re dealing with a call center, not someone who knows you and your situation.

Step 3: How to Look – Comparing Quotes and Companies Like a Pro

Okay, this is where most people mess up. They get a bunch of quotes, pick the cheapest one, and call it a day. Big mistake! Getting good insurance is like buying a used car – price matters, but it’s not everything.

What Information Do You Need to Get a Quote?

First, gather your info. For car insurance, you’ll need everyone’s driver’s license info, your car’s VIN, and your driving records. Yeah, that speeding ticket from three years ago still counts.

For home insurance, know your house details – when it was built, what it’s made of, square footage, all that good stuff. Got a security system or a new roof? Mention it – you might get discounts.

Don’t try to fudge the details to get a cheaper quote. Trust me, if you file a claim and they find out you lied about something, you’re gonna have a bad time.

Beyond Price: Factors to Compare

Here’s where we separate the smart shoppers from the bargain hunters who end up crying later.

Financial Strength matters big time. You want an insurance company that’ll be able to pay your claim, especially if it’s a big one. Look for A.M. Best ratings of A or better. Anything below that and you’re taking a gamble.

Customer Service is huge. J.D. Power does these ratings every year, and they’re worth checking out. You don’t want to find out your insurance company has terrible customer service when you’re dealing with a totaled car and need a rental ASAP.

Check out online reviews too, but take them with a grain of salt. Every company has some unhappy customers, but look for patterns. If everyone’s complaining about the same thing, that’s a red flag.

Discounts can add up to serious savings. Bundle your car and home insurance, be a good student, drive safely, install security systems – all that stuff can cut your bill. Some companies even have apps that track your driving and give you discounts for being a safe driver (though they’ll also know if you speed, so there’s that).

Step 4: Finalizing Your Choice – Reading the Fine Print

I know, I know – nobody wants to read insurance policy documents. They’re boring and full of legal jargon. But here’s the thing: that boring document is what determines whether you’re covered when stuff hits the fan.

Understanding Your Policy Documents

Premium = what you pay. Pretty straightforward. Pay annually if you can swing it – most companies give you a discount for that.

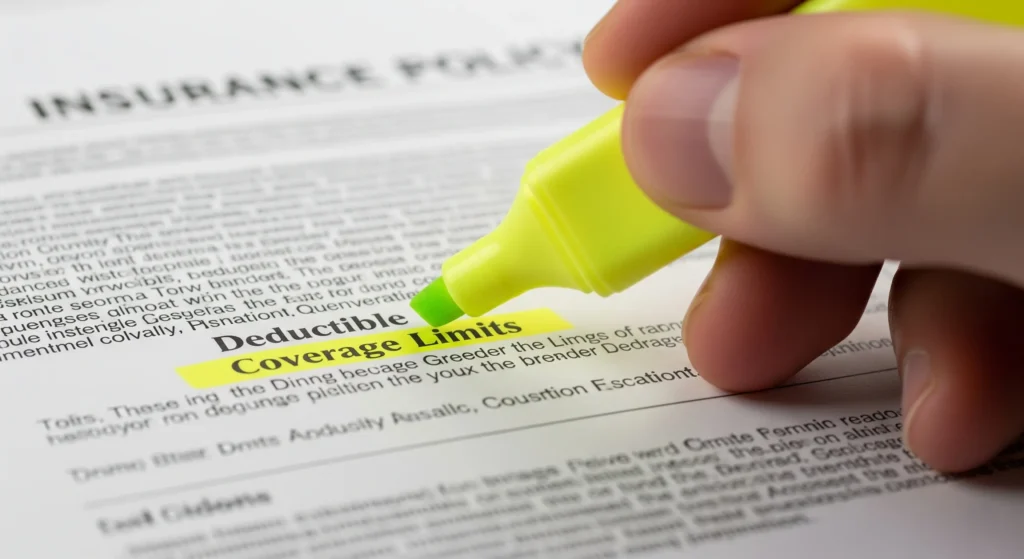

Deductible = what you pay before insurance kicks in. We talked about this earlier, but it’s worth repeating: don’t choose a deductible you can’t afford.

Coverage Limits = the most your insurance will pay. This is super important for liability coverage. If you cause an accident that costs $100,000 but you only have $50,000 in coverage, guess who’s paying the other $50,000? Yep, you.

Exclusions = what’s NOT covered. Every policy has them. Flood damage usually isn’t covered by regular homeowners’ insurance. Normal wear and tear isn’t covered. If you trash your stuff on purpose, that’s not covered either (obviously).

The Importance of a No-Claim Discount/Bonus

This is like a good behavior reward. Don’t file claims, and your rates go down over time. Some companies will cut your rates by 20-50% if you keep your nose clean for several years.

But here’s the thing – sometimes it makes sense to pay for small repairs yourself instead of filing a claim, especially if it’s just a bit more than your deductible. A $800 repair with a $500 deductible might not be worth filing a claim if it’s gonna mess up your no-claim discount.

Making a Claim: What to Do When the Unexpected Happens

This is the moment of truth – when you find out if you made a good choice or if you’re about to learn an expensive lesson.

A Step-by-Step Guide to Filing a Claim

First things first – make sure everyone’s safe. Take pictures of everything, get people’s contact info, and call the cops if needed. Don’t admit fault or start apologizing all over the place, even if you think it might be your fault.

Call your insurance company ASAP – like, within 24 hours if possible. Most companies have 24/7 claim hotlines, and many have apps that make reporting super easy. The sooner you report, the better.

Document everything – claim numbers, adjuster names, what people told you, when they told you. If it’s not written down, it didn’t happen. This stuff can drag on for weeks or months, and you’ll forget details.

Be cooperative but know your rights. Answer their questions honestly, but don’t feel like you have to accept the first offer if it seems low. You can negotiate.

How an Independent Agent Can Be Your Greatest Ally During a Claim

This is where having an independent agent pays off. They know how to work the system and can go to bat for you if the insurance company is being difficult.

Good agents have relationships with claim adjusters and know who to call when things get stuck. They can explain what’s happening, help you understand your options, and make sure you’re getting everything you’re entitled to.

It’s like having a translator and advocate rolled into one, and honestly, it can make the difference between a smooth claim experience and a total nightmare.

Frequently Asked Questions (FAQs) About Looking for Insurance

How often should I look for new insurance?

At least once a year when your policy renews, but also whenever your life changes significantly. Got married? Had a baby? Bought a house? Time to review your coverage.

Some people shop for car insurance every six months since rates change pretty frequently. It’s a bit of a pain, but hey, if you can save a few hundred bucks a year, it might be worth it.

Will looking for multiple insurance quotes hurt my credit score?

Nah, not really. Insurance quotes usually just do “soft” credit checks that don’t affect your score. It’s not like applying for a bunch of credit cards.

The money you could save by shopping around is way more important than any tiny ding to your credit score anyway.

What’s the biggest mistake people make when looking for insurance?

Going for the cheapest option without thinking about what they’re getting. I can’t tell you how many people I know who saved $200 a year on insurance only to get stuck with a $5,000 bill because their cheap policy didn’t cover what they needed.

It’s like buying the cheapest parachute you can find – probably not the best place to cut corners.

Can I trust online insurance review sites?

They’re helpful, but don’t take them as gospel. People are more likely to leave reviews when they’re angry, so you’re gonna see a lot of complaints.

Look for patterns and check multiple sources. And check out the professional ratings from J.D. Power and A.M. Best – those are more objective.

What’s the difference between liability and full coverage auto insurance?

Liability coverage pays for damage you cause to other people and their stuff. It’s usually the minimum required by law, but it won’t fix your car if you wreck it.

“Full coverage” adds comprehensive (covers theft, weather damage, vandalism) and collision (covers accident damage to your car). If your car’s worth more than a few thousand bucks, you probably want full coverage.

Why are my insurance rates different from my friend’s/neighbor’s?

Because you’re not the same person! Your age, driving record, credit score, where you live, what you drive – it all matters. Even small differences can add up to big rate differences.

Plus, different companies target different types of customers, so Company A might love you while Company B thinks you’re high risk. That’s why shopping around is so important.

Is the cheapest insurance policy always the best one to choose?

Nope, not. Cheap insurance is like cheap sushi – you might save money upfront, but you could regret it later.

Look for good value, not just a low price. Sometimes paying a little more gets you way better coverage and service. And trust me, when you’re dealing with a claim, you’ll be glad you didn’t go with the bargain-basement option.

Look, I get it – insurance isn’t exactly thrilling stuff. But taking the time to do it right can save you thousands of dollars and tons of stress down the road. Whether you end up with Look Insurance Agency or someone else entirely, just make sure you’re getting coverage that protects you, not just the cheapest thing you can find.

Think of good insurance like a boring superhero – you might not appreciate it day to day, but when disaster strikes, you’ll be really glad it’s there. And hey, once you get it sorted out, you can forget about it for a whole year!

Remember, the goal isn’t to win the prize for spending the least on insurance. The goal is to sleep well at night knowing that if something bad happens, you and your family are gonna be okay. That peace of mind? Worth a few extra bucks a month.